In a sign of rebounding confidence in Ghana’s financial landscape, the country’s banking industry reported significant expansions in deposits, loans, and operating assets last year, according to a new report by PwC.

The findings, part of the firm’s 2025 Ghana Banking Survey, highlight how established institutions like Ecobank Ghana (EBG) and GCB Bank are strengthening their dominance amid a push for digital innovation and regulatory adjustments.

Total industry deposits climbed 32.2 percent to 266.73 billion Ghanaian cedis (about $17 billion at current exchange rates) in 2024, up from 201.73 billion cedis the previous year.

This surge reflects broader efforts to boost financial inclusion, with banks leveraging extensive branch networks and digital platforms to attract a diverse clientele, from small businesses to tech-savvy young professionals.

Ecobank Leading The Pack

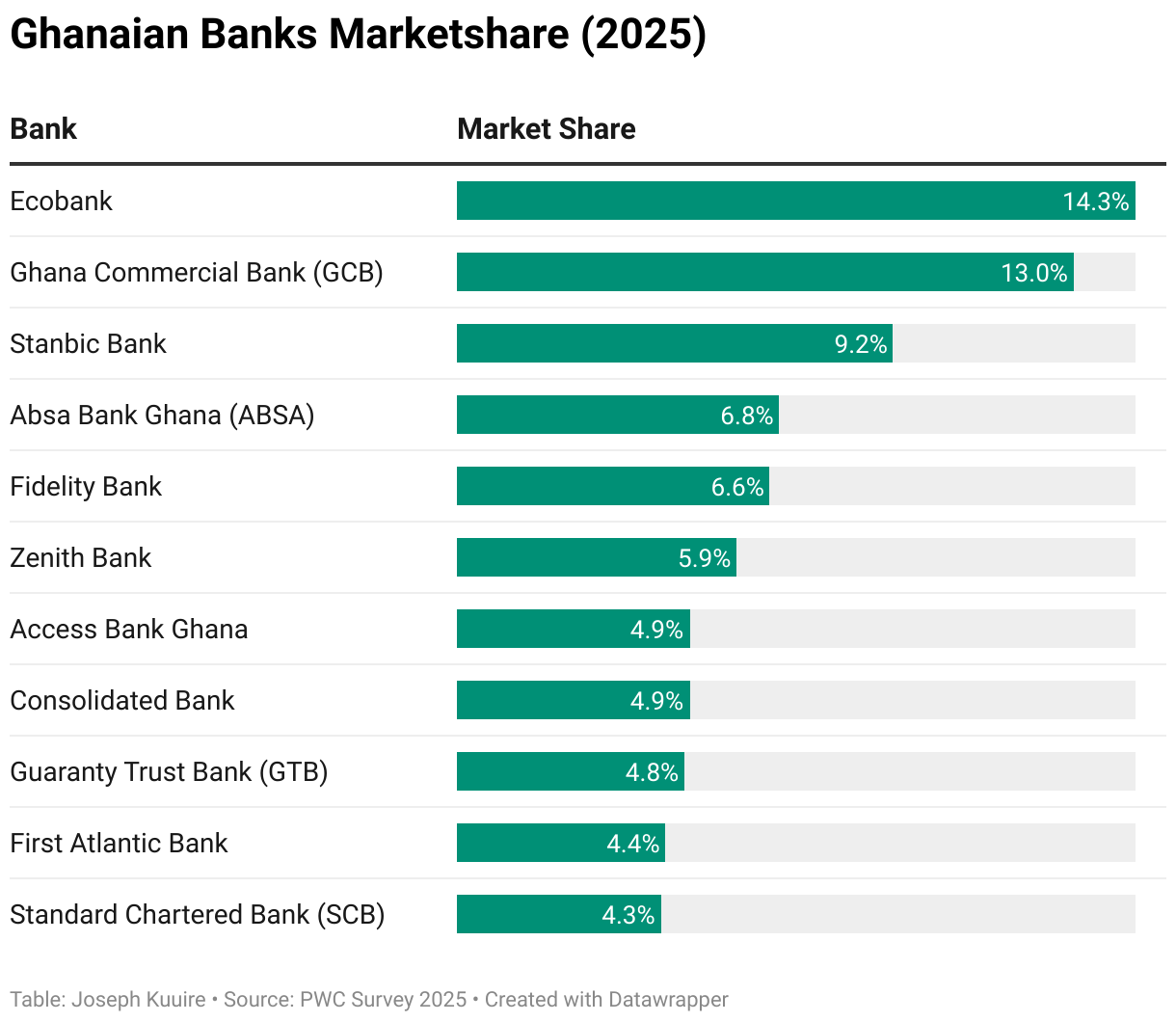

EBG and GCB led the pack, commanding a combined 27.3 percent of the market — an increase from 25.1 percent in 2023.

EBG held the top spot with 14.3 percent, while GCB followed at 13 percent. Their success stems from strategic moves like maintaining over 250 branches each nationwide, investing in mobile banking apps and offering tailored savings products for small and medium enterprises (SMEs) and salaried workers.

“Their longstanding reputations for reliability and service excellence continued to inspire confidence, especially in a macroeconomic environment that emphasized financial security,” the report noted.

Standard Chartered Bank Ghana/Stanbic (SBG) and Absa Bank Ghana (ABSA) rounded out the top four, with SBG at 9.2 percent and ABSA at 6.8 percent. Together, they grew their deposit bases by 6.9 billion cedis.

Mid-tier players showed dynamism: Access Bank Ghana (ABG) climbed from ninth to seventh place with 4.9 percent, and Guaranty Trust Bank (GTB) rose from 11th to ninth at 4.8 percent.

However, Standard Chartered Bank (SCB) slipped from seventh to 11th, at 4.3 percent, potentially due to competitive pressures.

Current Accounts and Lending

The growth wasn’t uniform across deposit types. Current accounts jumped 37.4 percent, savings accounts 44.2 percent, and interbank deposits nearly 50 percent — a nod to rising trust among institutions. Time and fixed deposits, however, dipped 6.2 percent, as customers favored more flexible options amid shifting interest rates.

Analysts attribute much of this momentum to the Bank of Ghana’s updated Cash Reserve Ratio (CRR) policy, which links reserve requirements to banks’ loan-to-deposit ratios (LDRs).

Banks with higher LDRs face lower reserves, incentivizing deposit growth to manage liquidity. Yet the report warns that without matching lending expansion, institutions could face profitability squeezes from elevated reserves.

On the lending side, gross loans and advances rose 26.6 percent to 85.18 billion cedis, with net loans reaching 73.7 billion cedis. This uptick signals a recovery from the constraints of Ghana’s 2022-2023 domestic debt exchange program, which had curtailed credit amid economic uncertainty.

GCB overtook EBG as the leader in advances, with 15.4 percent market share after a 60.3 percent year-over-year portfolio expansion. EBG held second at 14.3 percent, followed by ABSA at 11.5 percent and SBG at 10.6 percent. Standout performers included ABG, which grew its loans by 57.8 percent to claim 5 percent share, and ABSA with 33.6 percent growth.

The services sector absorbed the largest slice of credit at 16.7 percent, while commerce and finance took 15.8 percent — underscoring demand for short-term financing among SMEs.

Banks are increasingly using digital channels and fintech partnerships to reach underserved groups, such as informal traders and women-led businesses, via mobile apps and streamlined approvals.

“These collaborations enabled the seamless rollout of small and medium-sized loan products,” the report said, emphasizing a deliberate focus on financial inclusion.

Operating Assets

Operating assets — encompassing cash, liquid investments and loans — ballooned to 308.4 billion cedis, a 33.9 percent increase from 230.3 billion cedis in 2023. Cash holdings drove much of this, soaring 68.5 percent to 126.7 billion cedis, while liquid assets grew more modestly at 12.1 percent to 107.7 billion cedis.

EBG and GCB again dominated, with 13.6 percent and 13 percent shares, respectively. SBG followed at 10.1 percent. SCB’s slide continued here, dropping to 10th place at 4.3 percent. The top 10 banks controlled over half the market, affirming their sway.

This asset buildup, fueled by deposit mobilization, positions the sector for more agile responses to opportunities, the report suggests. However, it cautions that sustained vigilance on credit quality is essential to avoid rising defaults in a still-recovering economy.

PWC Survey Overview

The PwC survey, which draws on data from 20 banks, comes as Ghana’s economy shows signs of stabilization, with GDP growth hitting 5.7 percent in 2024.

While the report’s broader theme explores AI’s role in banking — from chatbots to fraud detection — the market share data underscores how digital tools are already reshaping competition, helping leaders like EBG and GCB pull ahead.

Bank executives interviewed for the survey expressed optimism but stressed the need for balanced growth. As one put it, in a nod to the CRR framework: “Maintaining rigorous credit assessments and portfolio monitoring will be critical.”

This article was edited with AI and reviewed by human editors