Story Highlights

- IMANI Africa has published documents showing that the State Interests and Governance Authority (SIGA) issued a formal directive in December 2025 instructing state-owned enterprises to prioritise insurance business with SIC Insurance PLC and SIC Life Company Limited.

- The directive’s subject line explicitly uses the word “directive” — directly contradicting SIC’s Managing Director, who told media the communications amounted to mere “encouragement.

- The government holds a minority stake in the publicly listed SIC Insurance PLC, creating a structural conflict: the state that regulates the insurance market and oversees SOEs is also a shareholder in the company now positioned to receive their business.

- IMANI founder Franklin Cudjoe has formally petitioned President Mahama. Industry veteran Sir Sam Jonah and insurer GLICO General have also raised alarms. The Presidency says it will take “appropriate action where required.

On December 11, 2025, the State Interests and Governance Authority (SIGA) issued a communication whose effect, if not always its tone, was unmistakable: state institutions were to prioritise insurance placements with state-linked insurers, specifically SIC Insurance PLC and SIC Life Insurance Ltd.

That single letter, now in the public domain thanks to documents released by the policy think tank IMANI Africa, has sparked one of the most significant debates in Ghana’s financial services sector in years.

It touches on the integrity of market competition, the boundaries of state oversight, the meaning of regulatory neutrality, and a structural conflict at the heart of Ghana’s public sector governance.

The Document That Started It All

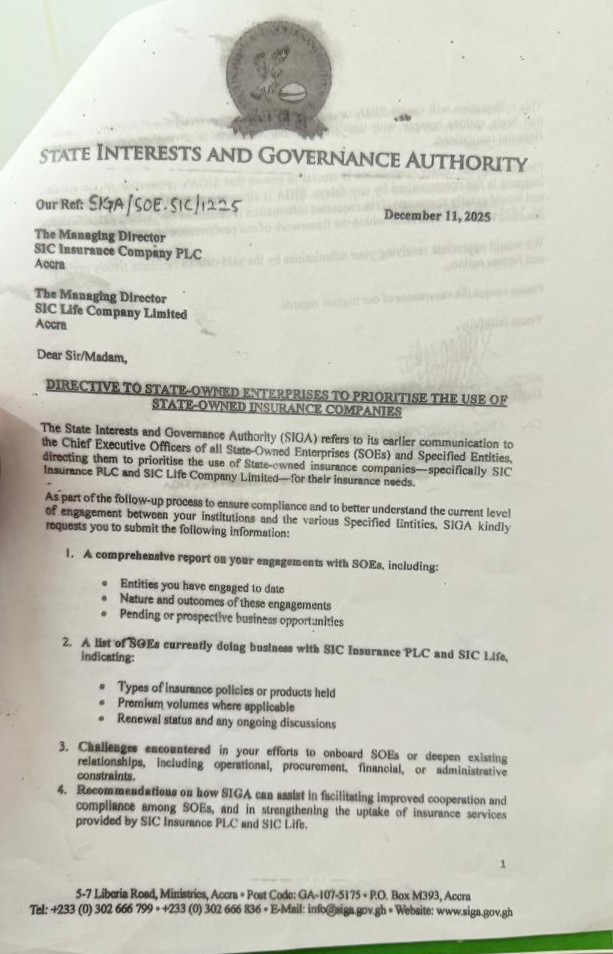

The documents, published by IMANI Africa as part of a new analysis titled The Insurance Question: Competition or Coordination?, centre on the December 11, 2025, letter from SIGA bearing reference number SIGA/SOE.SIC/1225.

The letter’s subject line leaves little room for interpretation: “Directive to State-Owned Enterprises to Prioritise the Use of State-Owned Insurance Companies.“

In the body of the letter, SIGA references an earlier communication sent to the Chief Executive Officers of all SOEs and Specified Entities, which it says was intended to get those institutions to prioritise SIC Insurance PLC and SIC Life for their insurance needs.

The December 11 letter was a follow-up, requesting compliance reports from SIC — including lists of SOEs already doing business with the company, premium volumes, and renewal status.

The compliance-monitoring aspect is particularly significant. Asking SIC to report back on which SOEs had followed the guidance, and what premiums had been generated, is not merely administrative encouragement.

Within weeks, the signal began moving through the system. A letter from SIC Life Insurance Ltd, dated December 23, 2025, addressed to GIHOC Distilleries, does not operate in isolation.

It explicitly references guidance from the Ministry of Finance and SIGA, and requests to be “favourably considered” in the institution’s renewal cycle. It is framed as a commercial request, but anchored in policy alignment.

That distinction matters. Because in a purely competitive market, no insurer needs policy backing to compete. It competes on price, underwriting strength, claims record, and reinsurance capacity.

But when policy begins to travel with the proposal, the playing field changes.

The Scale of What Is at Stake

To understand why this controversy has drawn attention from the highest levels of Ghana’s business community, one must appreciate the sheer size of the public sector insurance market.

SIGA’s own portfolio, as of its most recent reporting cycle, covers over 140 active entities, including 53 State-Owned Enterprises, 31 Joint Venture Companies, and multiple state-linked institutions across energy, finance, transport, and infrastructure.

These include the Ghana National Gas Company, Volta River Authority, Ghana Revenue Authority, and Cocoa Marketing Company.

Each of these institutions carries complex, high-value risk portfolios that run into hundreds of millions, and in some cases billions, of cedis in insured exposure.

Insurance at this level is not retail. It is structured finance. It determines which insurer leads, which local insurers participate, which international reinsurers commit capacity, and how risk is priced in global markets.

In practical terms, what SIGA appears to be attempting — or what, at minimum, its communications have triggered — is a consolidation of the country’s most lucrative and technically demanding insurance portfolios with a single cluster of state-linked insurers.

The knock-on effects on the competitive market, on international reinsurance arrangements already in place, and on the actuarial pricing of national risk, could be far-reaching.

Potential Conflict of Interest

What makes the arrangement especially sensitive is who owns whom.

SIC Insurance PLC is a publicly listed company. Government holds a minority stake, approximately one-third, while the majority of shareholders are private and institutional investors.

So when state institutions are guided toward SIC, they are not transacting internally within government. They are directing public business toward a commercial entity with mixed ownership.

The same state that oversees SOEs through SIGA and regulates the insurance market through the National Insurance Commission is, therefore, also a shareholder in the company now being positioned to receive that business.

This three-way overlap — regulator, overseer, and partial owner — is not automatically illegal. But it creates the kind of structural ambiguity that invites abuse and, at a minimum, demands the highest level of transparency.

The state, in effect, is potentially steering its own enterprises toward a company in which it has a financial interest, using its administrative authority to do so — all while wearing the hat of the neutral referee.

IMANI associate Kay Codjoe, who authored the analysis, frames the concern precisely: the question is not whether this is illegal by default, but where policy ends, and market interference begins.

The SIC Managing Director’s Problem

As the documents began circulating publicly, SIC Managing Director James Agyenim-Boateng found himself on the defensive.

He told JoyNews in an interview that SIGA’s communications amounted to encouragement, not a directive. It was a characterisation that might have held, had the documents not been available for anyone to read.

The December 11 letter, authored and signed by SIGA itself, uses the word “directive” in its subject heading and references compliance follow-up in its body.

The gap between the MD’s characterisation and the document’s actual language is not a minor semantic disagreement.

It goes to the heart of the public’s ability to trust the accounts of those managing state-linked enterprises when their interests are directly implicated.

SIGA Pushes Back

SIGA’s Director General, Dr. Michael Kpessa-Whyte, in an interview with Joy FM’s Newsnight on Wednesday, offered the authority’s most substantive defence yet.

Dr. Kpessa-Whyte explained that the letters were intended only to ensure SIC and SIC Life “remain at the table” during insurance competitions and were not meant to concentrate SOE insurance in their hands.

He further argued that IMANI’s account was incomplete. He said there is an earlier letter that was sent to SOEs and other specified entities, clarifying the role of state insurers, which had not been shared publicly.

That letter, he said, was encouraging heads of specified entities to ensure that SIC and SIC Life, as the state insurers, stay at the table whenever there is insurer competition.

Dr. Kpessa-Whyte said that after a subsequent meeting involving SIGA, SIC, SIC Life, and private insurers, all parties understood the guidance, and there was no issue of monopolisation.

He also suggested that some private insurers may have misrepresented the letters, and noted that SIGA plans to identify those who have done so publicly.

The defence is coherent in outline. But it runs up against a fundamental problem: if the intent was merely to ensure SIC and SIC Life participated in competitive tenders, why was the follow-up letter framed around compliance tracking, premium volumes, and renewal confirmations?

Industry Voices Grow Louder

Across parts of the system, insurers outside the SIC structure are reporting non-renewal of existing policies, reduced participation in state-linked risk placements, and sudden shifts in engagement patterns.

GLICO General Insurance, one of Ghana’s most established non-life underwriters, has gone further than most. Led by A. Achampong-Kyei, the company formally wrote to the President.

He raised concerns about the disruption of established insurance placements, the reallocation of portfolios without competitive assessment, the role of third-party engagements in international reinsurance, and market distortion and regulatory neutrality.

Sir Sam Jonah, an industry veteran, had previously described the pattern as “deeply troubling and dangerously systemic.”

The Petition and the Presidency

IMANI founder Franklin Cudjoe formally petitioned President Mahama on the issue last Tuesday, warning of “unseen political hands” raiding the insurance sector through administrative directives.

The government has said President Mahama will review the IMANI petition and take “appropriate action where required.”

The question now is whether the review will be substantive, resulting in a clear statement on competitive policy and the limits of SIGA’s mandate, or procedural, producing little more than assurances.

What Comes Next

The real question is this: Is Ghana deliberately restructuring its insurance market to consolidate state-linked participation, or is the system drifting into that position without fully confronting the consequences?

Because if it is the former, then it must be justified clearly, legally, and transparently. And if it is the latter, then it must be examined before it settles into permanence.

There is also a broader governance question that this episode has made visible.

Ghana’s state oversight architecture — SIGA, the National Insurance Commission, the Ministry of Finance — is built on the assumption that each institution plays a distinct and bounded role.

The documents IMANI has released do not prove corruption. They do not establish that the Mahama administration authorised a takeover of the insurance market.

But they do establish that something happened — that directives were issued, that compliance was monitored, that commercial letters followed, and that market participants began to feel the effects.