Story Highlights

- Ghana’s pension industry has grown dramatically, but only a fraction has been deployed into private equity and venture capital

- Ghana became the first African country to mandate a minimum 5% pension fund allocation to domestic private equity and VC — potentially unlocking over $300 million annually

- Speakers at the 2026 GVCA Annual Conference identified a “crisis of confidence” — not a lack of capital — as the root cause of underinvestment

ACCRA, GHANA — There is no shortage of capital in Ghana. That much was agreed upon before the first panel had even begun at the 2026 Ghana Venture Capital and Private Equity Association (GVCA) Annual Conference, held on Wednesday, 23rd April in Accra.

The conference, themed “Fueling Ghana’s Future Through Domestic Alternative Investments and Unlocking Trapped Capital”, convened fund managers, pension fund administrators, development finance institutions, regulators, and entrepreneurs under one roof — united by a single, uncomfortable question: Why, in a country with a booming pension industry, are local businesses still starved of growth capital?

A Growing Pot, An Empty Pipe

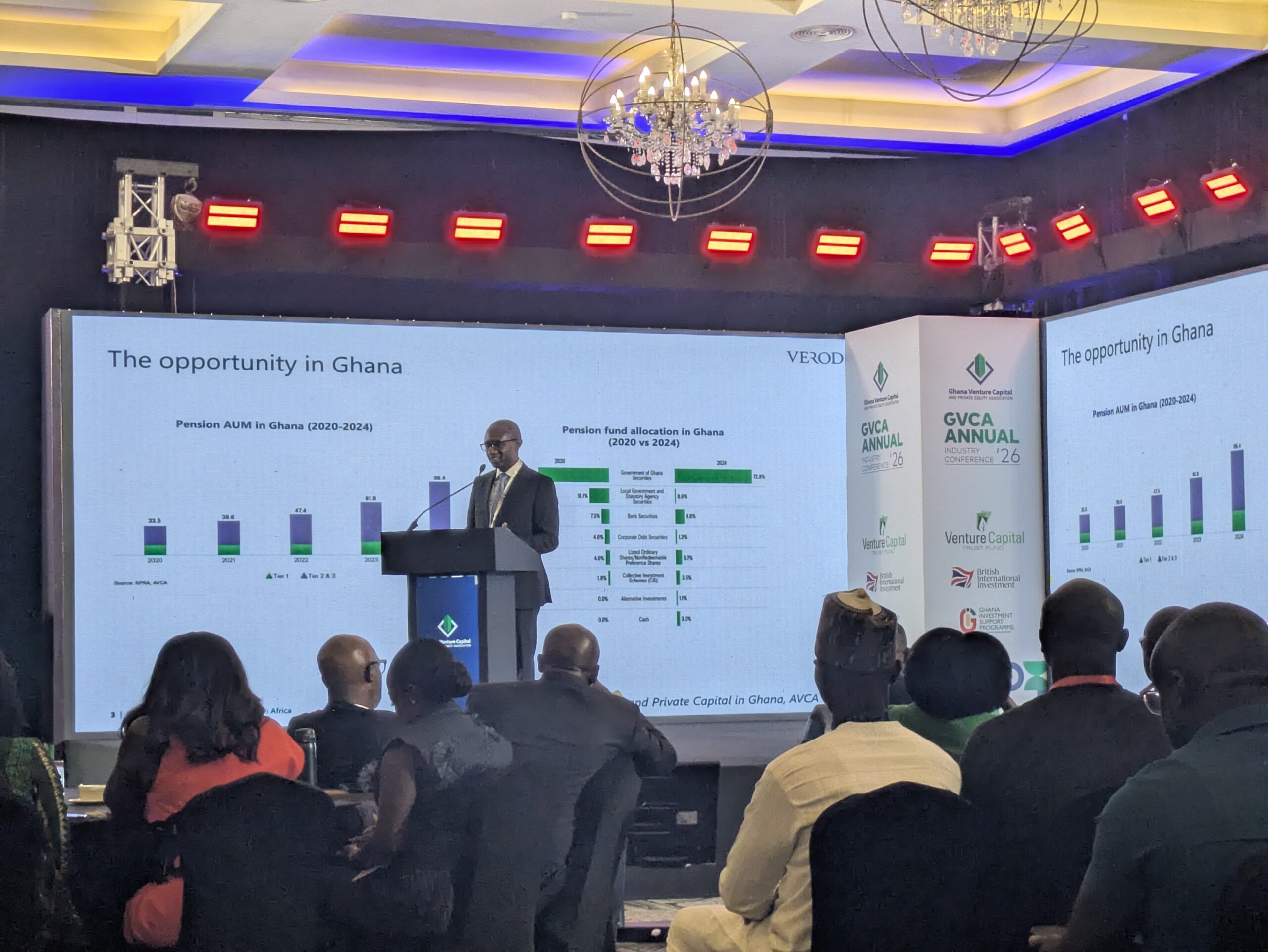

Ghana’s pension sector has expanded significantly over the past decade. Despite allowing up to 25% of pension assets to be invested in alternative funds, only 0.58% was actually allocated before the government’s landmark directive.

“Domestic capital needs the right information, the right governance, and the right amount of confidence,” said Danladi Verheijen, co-founder of Verod Capital and a representative of the African Venture Capital Association (AVCA), which serves as an oversight body for private capital across the continent.

Speaking at the conference, Verheijen drew a sharp distinction between capital that is absent and capital that is simply paralysed.

A Crisis of Confidence, Not Capital

Michael Abbey, Chief Executive of the Venture Capital Trust Fund (VCTF) — Ghana’s government-backed domestic alternative investment vehicle — offered what may have been the conference’s most pointed diagnosis.

The problem, he argued, is not appetite. It is trust.

“It may be a crisis of confidence,” Abbey said in his address. “A systemic distrust between capital and entrepreneurship that decades of failed interventions have only deepened.”

He pointed to a collective scar tissue accumulated from failed startups, defaulted loans, and promising enterprises that collapsed not from bad ideas but from an inability to access working capital at critical moments.

“We cannot lecture our way back from this problem,” he said. “We must earn that trust — through transparent data, good and enforceable contracts, through exits that actually deliver returns to local investors.”

Abbey’s remarks struck at a well-worn tension in African private capital: the expectation that domestic investors — particularly pension funds and family offices — should commit patient, long-term capital to illiquid assets, while the broader ecosystem has rarely demonstrated the kind of track record that would justify that leap of faith.

The 5% Mandate: A Turning Point?

One policy development loomed large over the day’s discussions. Ghana became the first African country to mandate that local pension funds invest at least 5% of their assets in domestic private equity and venture capital firms.

With over $6.7 billion in pension deposits, this directive could unlock a $337 million funding pool for Ghanaian firms by the end of 2026.

The mandate has been celebrated by industry players as a structural breakthrough — but not without caveats.

Countries like Nigeria, Botswana, and South Africa also have regulations that cap how much pension funds can allocate to alternative investments.

However, those caps have largely failed to incentivise actual investment, with many African pension portfolios remaining heavily skewed toward government bonds and bank deposits.

Ghana’s distinction, advocates argue, is that this is a floor, not a ceiling — and therein lies the difference.

Matthew Adjei, CEO of Oasis Capital Ghana Limited, framed the moment with clear-eyed pragmatism.

“Capital repels three things,” he told delegates. “Trust — built through governance, transparency and performance. Once we perform and build a track record, we will build the trust that is required.”

He added that without credible exit pathways for investors, capital would always remain cautious, regardless of the regulatory framework.

Three Levers to Unlock Domestic Capital

Danladi Verheijen, drawing on 17 years of private equity investing across approximately 20 African companies, outlined three structural levers that could meaningfully shift domestic capital allocation.

The first is regulatory reform. He welcomed Ghana’s increase in the headline allocation ceiling for alternatives to 25%, but flagged persistent friction points: slow fund registration processes, absent or inadequate limited partnership legal structures, and double taxation concerns that continue to deter local fund formation.

The second is anchor investors — large, credible institutions willing to write the first cheque into a new fund, providing the signal that draws others in.

Development Finance Institutions (DFIs) have historically played this role, and Verheijen offered them explicit credit. “Without the DFIs, our industry would not exist,” he said.

But he argued the baton now needs to pass — at least partially — to domestic institutional capital.

The third lever is pooling. Rather than each pension fund building out internal private equity capabilities from scratch, Verheijen advocated for consortium investing: grouping domestic institutions together to co-invest alongside experienced managers who already understand how to evaluate, monitor, and exit private market positions.

Momentum, but Concentration

The conference took place against a backdrop of cautious optimism for African private capital more broadly.

African tech startups raised a combined $4.1 billion in equity and debt financing in 2025, marking a 25% increase year-on-year and the strongest funding year since 2022.

But the distribution of that capital remains deeply skewed. The top four markets — Nigeria, Kenya, South Africa, and Egypt — absorbed 72% of total capital, a figure that has remained largely consistent since 2019.

For Ghana, and for smaller ecosystems across the continent, the structural question is how to break into a funding landscape that has calcified around a handful of cities.

One encouraging data point emerged from Verheijen’s presentation. Between 2022 and 2025, allocations to the African private sector from domestic investors increased by approximately 30% — from around 15% to 21% of total allocations.

“It feels like a low number,” he acknowledged, “but it’s increasing dramatically.”

He also highlighted the growing role of sovereign wealth funds, noting that more are beginning to back African enterprises — a shift he described as both financial and political.

“Why is African capital going to build hospitals in Poland and tech companies in Silicon Valley?” he asked.

“If we’re not investing in our own companies, manufacturing our own drugs, and building our own infrastructure, we become dependent — and dependence has a cost.”

Focus on Action

The conference’s opening voice belonged to Amma Gyampo, CEO of GVCA, who set the tone with deliberate brevity. “The one question I want you all to take away into every session is: since last year, what have we actually done?” she told delegates. “There’s a lot of fatigue around talk and conferences. We are here to act.”

It was a pointed reminder that the diagnosis of Ghana’s trapped capital problem is no longer new. The policy architecture is increasingly in place.

Ghana now has 32 venture capital funds with a combined portfolio of 358 companies.

The pension reform is law. The institutional interest, at least in the room, appeared genuine.

This article was edited with AI and reviewed by human editors