Not long ago, I was behind a rickety pickup truck making its slow way through Accra’s morning traffic.

Branded with the name of a local security company, the vehicle was not ferrying gear or young guards, but half a dozen elderly men, grey-haired, thin, and slumped together in the open bucket

They were heading toward the old head office of the National Pensions Regulatory Authority. Each looked well above 65. None looked like they should still be working.

But they must work.

Growing old in Ghana is no shield from poverty. According to the 2021 Population and Housing Census report from the Ghana Statistical Service, 25.7% of Ghanaians aged 60 and above are multidimensionally poor.

That means they lack not only money but access to healthcare, education, and basic living conditions.

Surviving Life After 65

The average Ghanaian relies on roughly four strategies to fund life after 65. The first is savings and investments in farmland, housing, small businesses, or modest financial instruments.

However, this option is viable only for the minority with consistent earnings.

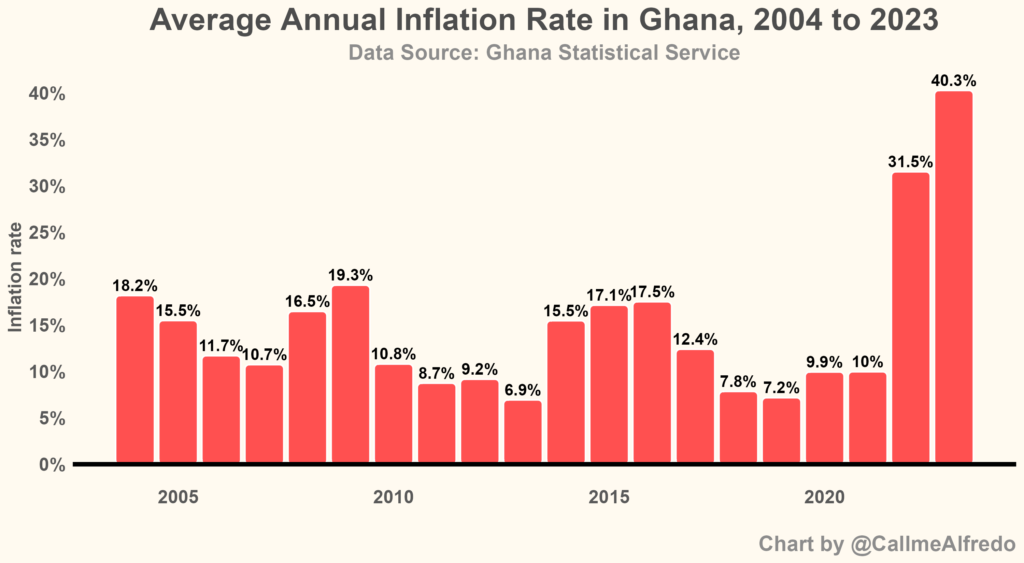

For most, saving is aspirational. Ghana’s inflation rate, which hovered around 20% over the past year, continues to erode value. Access to formal investment vehicles remains limited, especially in rural areas, and real estate may offer security, but not liquidity.

The second strategy is simple: keep working. According to the Ghana Statistical Service, 37.5% of elderly Ghanaians are still employed. Among them, 90.1% work in the informal private sector, of which more than half (53.2%) are classified as being in “vulnerable employment”.

The third option is participation in a formal pension scheme. SSNIT, the public tier of the 3 tier pension scheme, offers relatively stable income for those who contributed regularly.

As of 2023, only about 13.7% of Ghana’s total working population contributes to the SSNIT pension scheme. This figure is derived from the Ghana Statistical Service’s report, indicating a labor force of approximately 13.9 million individuals, and SSNIT’s report of over 1.9 million active contributors.

However, only about 12% of the total working population contributes to the scheme.

The voluntary tier, meant for informal workers, has seen slow uptake. Reasons range from lack of awareness and distrust of state institutions to immediate financial pressures that crowd out long-term thinking.

The idea that pensions are for office workers must be retired. Universal pensions, while appealing in theory, face the twin hurdles of limited fiscal space on the national budget and the risk of moral hazard

Lastly, there is the family. In Ghanaian tradition, adult children are expected to support their ageing parents. For years, this system worked as an informal safety net.

But high youth unemployment, rising cost of living, and urban migration have weakened these bonds. Some elderly Ghanaians now live alone, without regular remittances or reliable companionship.

What once was a cultural guarantee has become a gamble.

Fixing The Problem

Tackling old-age poverty in Ghana will require a rethink of both policy and perception. The first step is public education.

Formal pension schemes must be made ubiquitous across the working population, not only for civil servants and salaried employees, but also for artisans, traders, and the self-employed.

The idea that pensions are for office workers must be retired. Universal pensions, while appealing in theory, face the twin hurdles of limited fiscal space on the national budget and the risk of moral hazard.

Contributions, not entitlements, must remain the bedrock of the system.

Second, the structure of the basic national pension demands reform. At present, disparities in payouts are stark. Some retirees collect close to GHS 200,000 a year, while others receive just GHS 300 per month, below Ghana’s 2024 monthly minimum wage of GHS 456.

A progressive structure, with defined minimum and maximum thresholds, would better reflect a society committed to equity without punishing those who contributed more.

The image of those elderly men, rattling toward work in the open bed of a pickup, is not an anomaly. It is a mirror. A mirror held up to a society where savings vanish, pensions exclude, work never ends, and family is no longer a guarantee.

Their quiet presence in traffic, anonymous but dignified, forces a harder look at what Ghana asks of its elders and what it refuses to give.

If this is how the country treats those who built it, then what future does it offer those who will grow old next?